Something unusual is happening in Omaha real estate. Inventory is slipping, mortgage rates have moved higher, affordability is still tight, and yet sales activity is showing signs of life. That combination can feel confusing if we are trying to make sense of the market.

The good news is that the Omaha real estate market is not falling apart. It is adjusting. And when we look at the numbers across Douglas and Sarpy County, the story becomes a lot clearer.

Table of Contents

- Where we are measuring the market

- Inventory is down but the story is mixed

- Home prices are softening not crashing

- Sales are improving from depressed levels

- Months of supply still favors sellers

- Price per square foot and what it tells us

- Interest rates are still the big pressure point

- Jobs and inflation still matter

- What this means for buyers and sellers

- FAQ: Omaha Real Estate

Where we are measuring the market

For this snapshot of Omaha real estate, we are looking at Douglas and Sarpy County. That includes Omaha along with nearby communities like Ralston, Bennington, Waterloo, and Valley in Douglas County, plus Bellevue, Papillion, La Vista, Gretna, and Springfield in Sarpy County.

That matters because real estate is local. National headlines may be loud, but they do not always reflect what is happening here. Omaha is not Austin. It is not Phoenix. It is not a coastal boom and bust market. Omaha real estate follows its own path.

Inventory is down but the story is mixed

Total inventory across Douglas and Sarpy County is sitting at 1,853 homes, down 3 percent from last year. On the surface, that sounds simple enough. But once we split the market into new construction and existing homes, the picture changes.

- New construction: 837 homes, down 8.4 percent

- Existing homes: 1,015 homes, up 2.2 percent

The drop in new construction is a big part of the story in Omaha real estate. Builders are extremely sensitive to interest rates. When financing gets more expensive and buyer demand cools off, they tend to slow production. Carrying unsold homes costs money, and builders know it.

There is also a local factor. Celebrity Homes, a long time local builder, was recently acquired by D.R. Horton. That kind of transition can affect the pace and flow of inventory.

Even with that slowdown, the market has not stopped. People still need a place to live. Higher rates may tap the brakes, but they do not shut the whole thing down.

Home prices are softening not crashing

This is the question everybody asks about Omaha real estate. Are prices going to crash?

No.

Can prices flatten out or dip a little? Absolutely. In fact, that is exactly what we are seeing.

The median sale price last month in Douglas and Sarpy County came in at $330,000, down 1.5 percent from the same period last year.

That is not a reason to panic. A little moderation can actually help with affordability. And affordability is still one of the biggest issues in Omaha real estate.

When we break pricing out by property type, we see a sharper difference:

- New construction median price:$434,373, up 3.4 percent

- Existing home median price:$300,000, down 1.2 percent

That tells us a few things. First, new construction remains expensive. Second, existing homes are carrying more of the affordability burden. Third, small dips in price do not automatically mean danger. Markets correct. They breathe. That is normal.

We are also seeing households adapt. One recent example was a multigenerational purchase in Elkhorn, where multiple generations planned to live under one roof. When housing gets expensive, buyers do not always disappear. Sometimes they simply get more creative.

The basic long term formula still holds up:

- Buy what we can afford

- Take care of the property

- Stay put for at least five years

Historically, that approach has worked a lot better than trying to perfectly time Omaha real estate.

Sales are improving from depressed levels

One of the more encouraging signs in Omaha real estate is that closed sales increased last month.

A total of 961 homes closed, up 8.8 percent year over year.

Breaking that down further:

- New home sales: 192, up 13.6 percent

- Existing home sales: 769, up 7.7 percent

That is important because the market took a major hit after rates jumped in 2022. On a 12 month rolling average, sales are still well below pre pandemic levels. So yes, there was a real sales crash. But the recent movement is in the right direction.

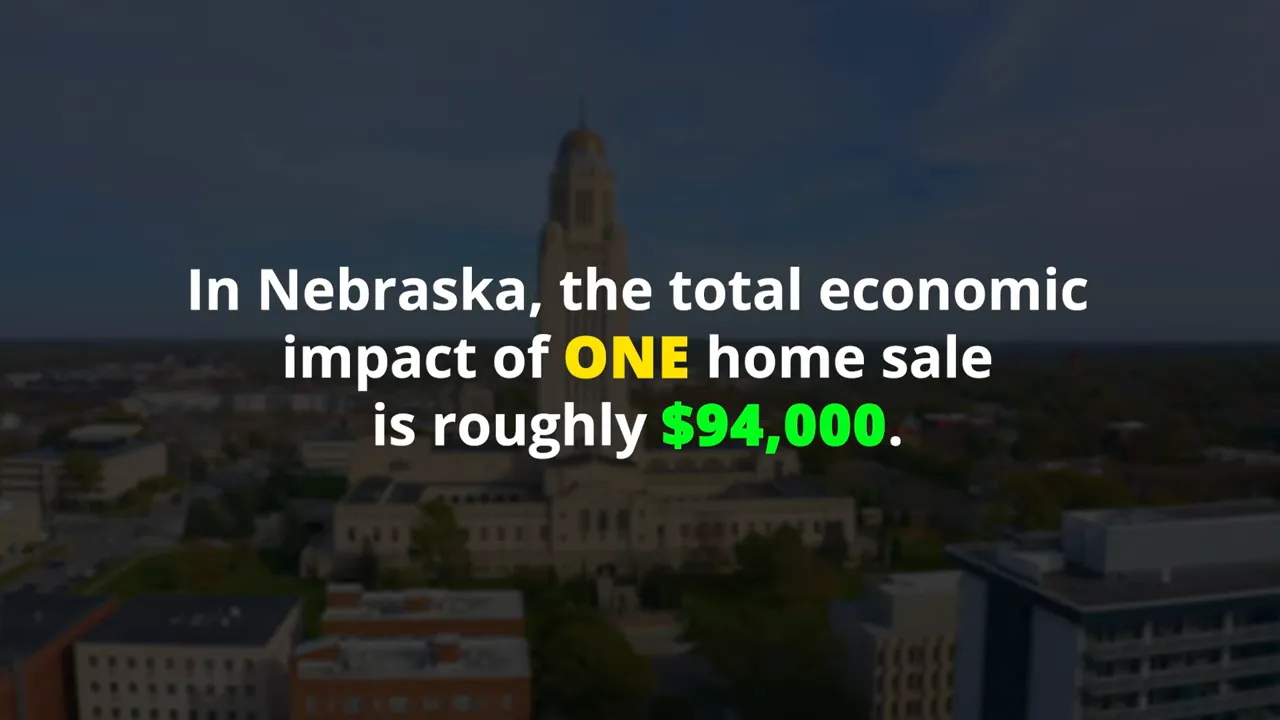

More transactions are healthy for the broader economy too. In Nebraska, the economic impact from a single home sale is roughly $94,000. Home sales ripple outward into lending, insurance, moving services, repairs, furnishings, contractors, and local spending.

Months of supply still favors sellers

If we want one quick way to understand market pressure in Omaha real estate, months of supply is a good place to start.

On the existing home side, the market currently has 1.3 months of inventory. In plain English, if no new homes came on the market, we would burn through current supply in about 1.3 months.

That is still firmly a seller's market.

- 1 to 3 months: seller's market

- 4 to 6 months: balanced market

- 6 months or more: buyer's market

That is why clean, well prepared, properly priced homes are still moving quickly in Omaha real estate. If a property is sitting, there is a good chance the pricing is off.

And if a seller needs to reduce the price, tiny cuts usually do not move the needle. A meaningful adjustment creates attention. A one percent discount rarely changes buyer behavior.

Price per square foot and what it tells us

Looking at the 12 month rolling average over the last five years, new construction is averaging $261 per square foot, while existing homes are averaging $217 per square foot.

That spread reinforces what many buyers already feel in the field. New homes offer fresh finishes and modern layouts, but they come at a premium. Existing homes continue to provide the more budget friendly entry point in Omaha real estate.

Interest rates are still the big pressure point

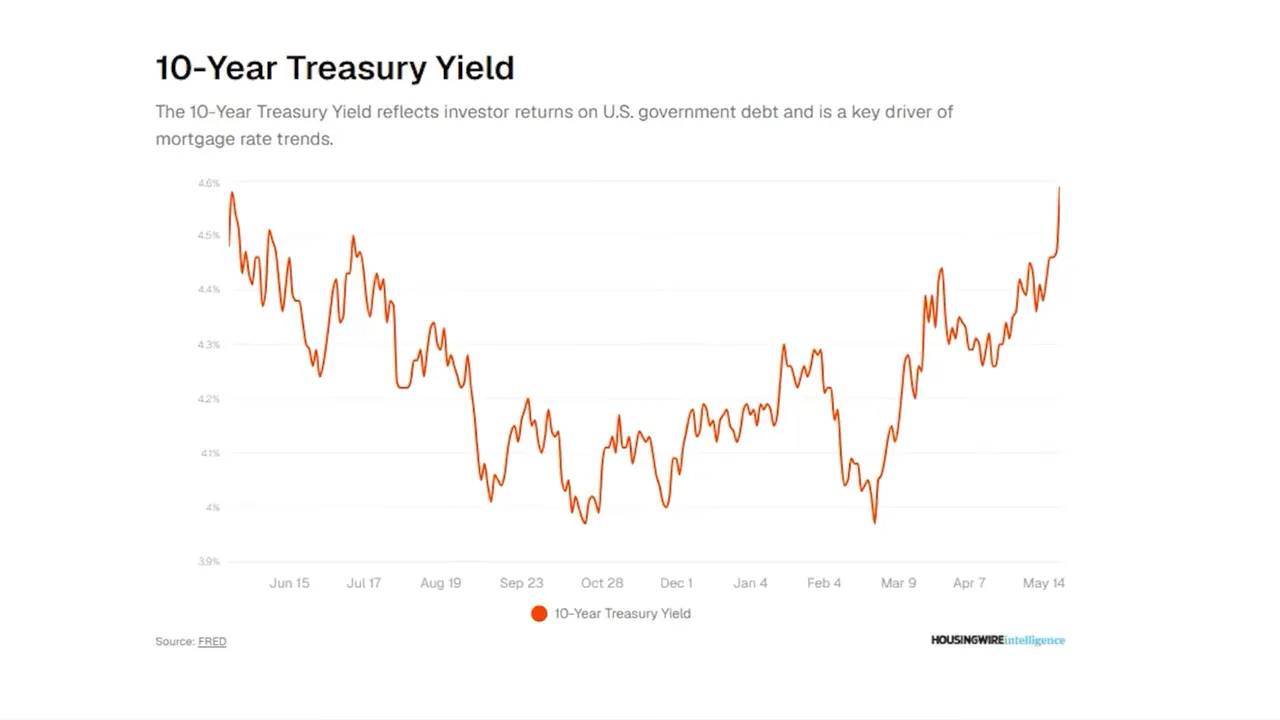

If there is one factor shaping Omaha real estate more than any other right now, it is mortgage rates.

Rates are currently above 6.5 percent, sitting around 6.75 percent. Earlier in the year, rates had dipped below 6 percent. Since then, they have climbed again.

That matters because payment shock is real. On a $300,000 loan, a 75 basis point increase adds roughly $150 per month. That is enough to push some buyers out of the market or force them to lower their target price.

Mortgage rates tend to track the 10 year Treasury yield, and the difference between those two numbers is called the spread. The spread has actually improved compared to the previous two years, which is one reason rates are not even higher.

One more reality check. The era of 3 percent mortgages is not coming back anytime soon. Historically, a rate around 6.75 percent is not bizarre at all. It only feels shocking because we got used to a temporary period of ultra cheap money.

That is why waiting for rates to collapse can turn into a long and frustrating game. If buying makes sense for our finances and our time horizon is five years or more, trying to outguess the next quarter of Omaha real estate may not be the best strategy.

Jobs and inflation still matter

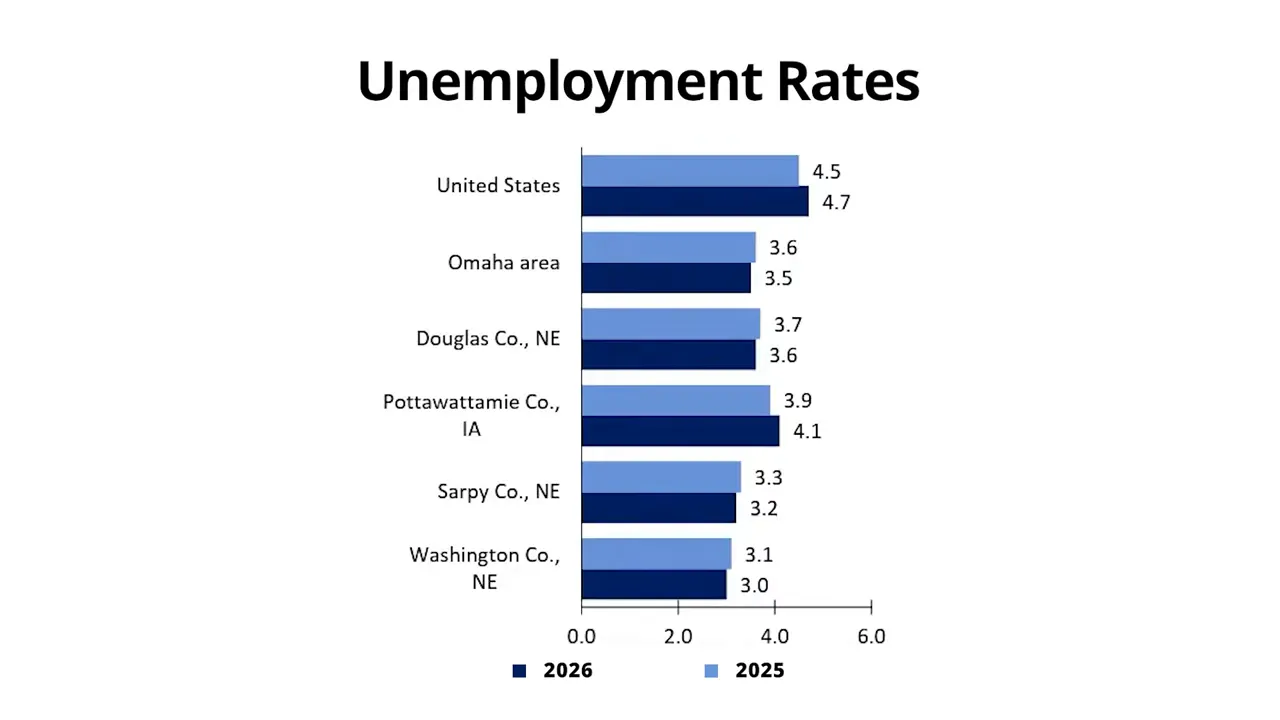

Housing demand does not exist in a vacuum. Employment and inflation both matter to Omaha real estate.

National unemployment is at 4.7 percent, up from 4.5 percent a year ago. Locally, Douglas County is at 3.6 percent and Sarpy County is at 3.2 percent.

Those local numbers are still relatively strong, and low unemployment generally supports housing demand.

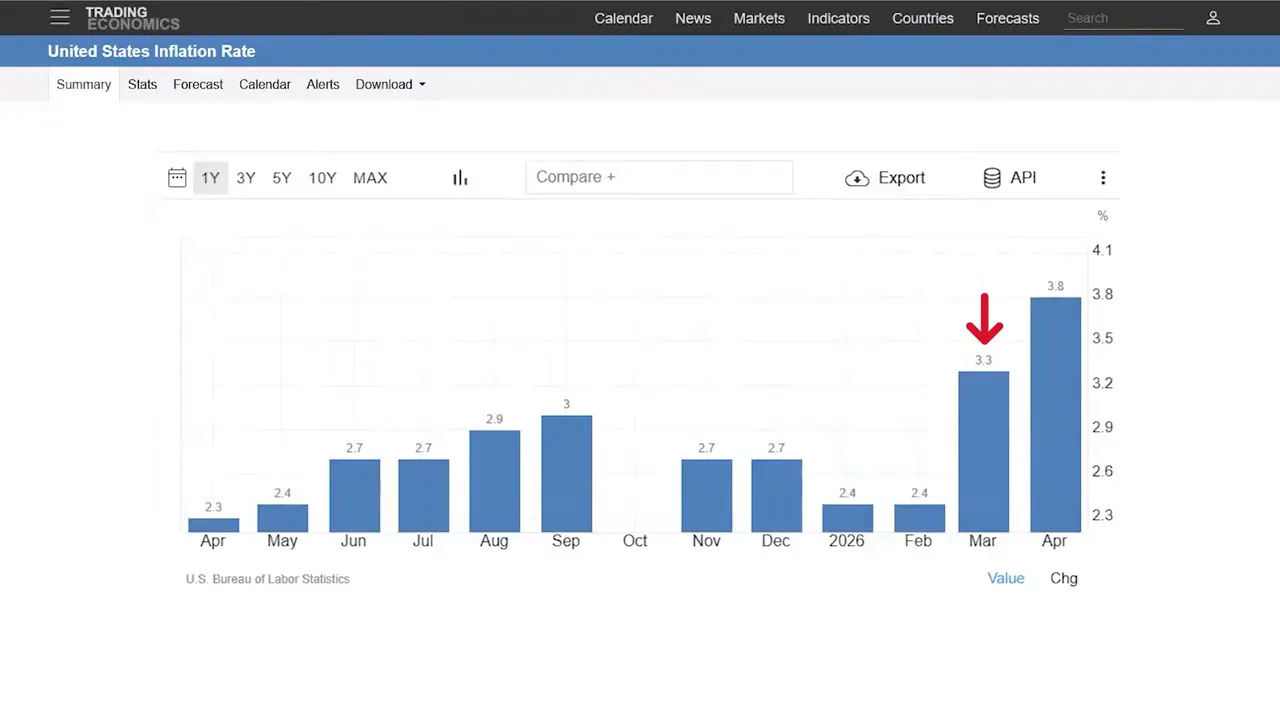

Inflation, on the other hand, has been heating back up. March came in at 3.3 percent and April rose to 3.8 percent.

When energy prices rise, everything from transportation to groceries to construction gets more expensive. And when inflation stays elevated, the Federal Reserve is more likely to keep rates higher for longer.

What this means for buyers and sellers

So what should we do with all of this?

For buyers in Omaha real estate, the key is to focus on readiness, not headlines. If we are financially prepared, buying for the right reasons, and planning to stay put long enough, this market can still work.

For sellers, the lesson is simple. Presentation and pricing matter more than ever. A home that is clean, staged, market ready, and priced right can still move quickly. A home that misses the mark may sit.

And for everyone else, the big takeaway is this: Omaha real estate is not breaking. It is recalibrating. Inventory is tight. Rates are painful. Affordability is strained. But sales are moving, local employment is solid, and prices are behaving much more like a normal market than a collapsing one.

That may not be dramatic enough for the headlines, but it is usually the kind of reality that helps us make better decisions.

If you’re considering buying, selling, or relocating in Omaha, I’d love to help you sort through what the numbers mean for your specific situation. Call or text me at 402-490-6771 to book a quick consultation.

We can talk through pricing, neighborhoods, and next steps so you feel confident moving forward—especially while rates and inventory are still shifting.

FAQ: Omaha Real Estate

Is Omaha real estate in a crash right now?

No. Omaha real estate is dealing with higher rates, low affordability, and softer pricing in some segments, but that is not the same thing as a crash. Small year over year declines are showing up, yet the overall market still has low inventory and rising closed sales.

Are home prices dropping in Omaha?

Median prices have eased slightly. The combined median sale price in Douglas and Sarpy County was $330,000, down 1.5 percent from last year. Existing homes were down 1.2 percent, while new construction was up 3.4 percent. That looks more like moderation than a major decline.

Is Omaha still a seller's market?

Yes. The existing home market has about 1.3 months of supply, which still falls in seller's market territory. Well priced homes in good condition are continuing to sell quickly.

Should we wait for mortgage rates to come down before buying?

That depends on personal finances and timing, but waiting for a perfect rate can be risky. Rates may come down later, or they may stay elevated longer than expected. In Omaha real estate, buying tends to make the most sense when the payment is manageable and the plan is to stay in the home for at least five years.

Why are new construction homes more expensive in Omaha?

New homes carry higher construction costs, regulatory costs, and financing sensitivity. In this market, the median new construction sale price is much higher than the median existing home price, and the price per square foot is also significantly higher.

Read More: