If you are moving to Omaha and thinking about buying your first home, it can feel like a lot all at once. Money, lenders, contracts, inspections, appraisals, closing costs, school districts, insurance, wire fraud, timelines. It is easy to get overwhelmed fast.

The good news is the process is a lot more manageable when you break it into clear steps. That is exactly what this guide does. Whether you need a practical Omaha homebuying guide or you simply want to understand how the process works before making a move, here are the 10 essential steps that can help you avoid expensive mistakes and make smart decisions.

Table of Contents

- Plan Your Finances Before Moving To Omaha

- Hire The Right Realtor For Moving To Omaha

- Get Preapproved The Right Way

- House Hunting Strategy For Moving To Omaha

- Make A Smart Offer Without Overcomplicating It

- Protect Yourself During Due Diligence

- Understand The Appraisal Process

- Do A Thorough Final Walkthrough

- Close The Right Way And Avoid Fraud

- FAQ

Plan Your Finances Before Moving To Omaha

Before you start scrolling through listings, you need to know what your money situation really looks like. If you are moving to Omaha, this is the foundation of everything else.

You need three buckets of money:

- Down payment

- Closing costs

- Emergency fund

Your down payment is the upfront money you put toward the purchase price. For example, an FHA loan typically requires a minimum of 3.5% down. On a $300,000 home, that is $10,500.

If you do not have enough saved for the down payment, there may be assistance programs available. In Nebraska, one example is NIFA, the Nebraska Investment Finance Authority. There are programs that can help finance the down payment over time, so it is worth exploring if cash upfront is your biggest obstacle.

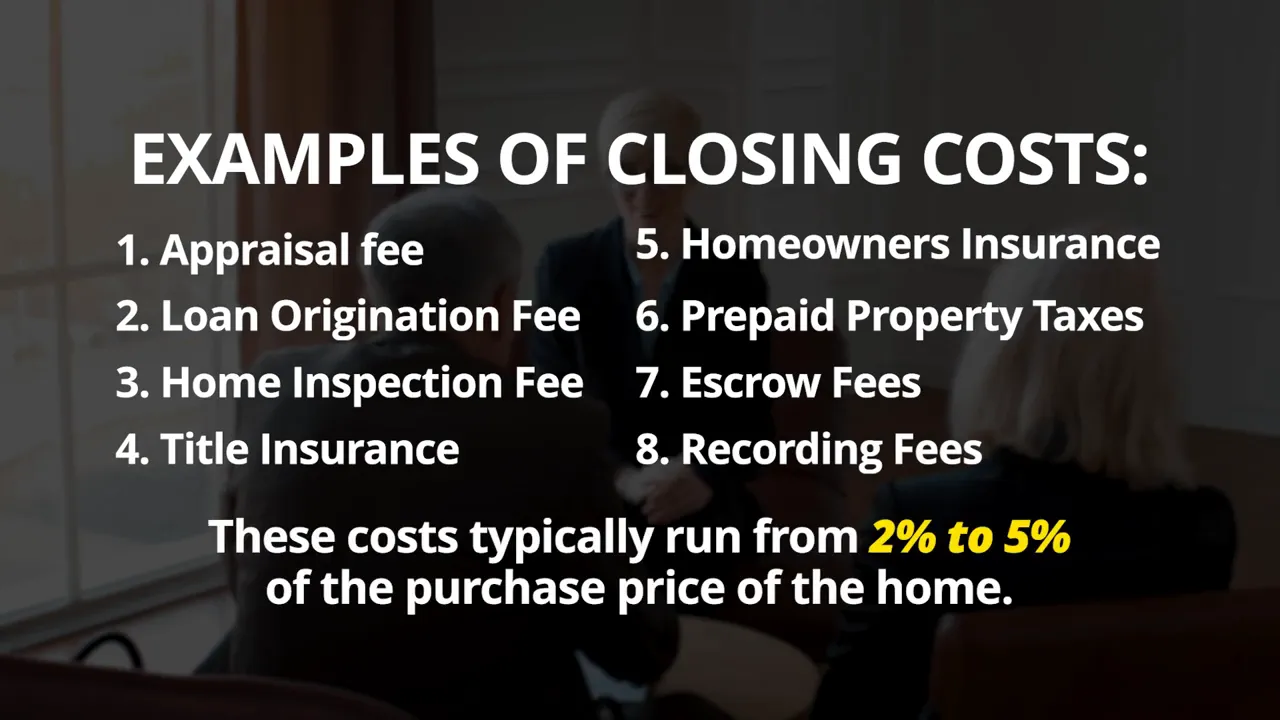

Then there are closing costs. These are the fees and prepaid expenses needed to finalize the purchase. Think appraisal fee, loan origination fee, home inspection, title insurance, homeowner's insurance, prepaid property taxes, escrow fees, and recording fees. A solid estimate is usually 2% to 5% of the home price.

Using 3% as an example, a $300,000 home would need about $9,000 in closing costs.

If you are short on closing costs, you may be able to ask the seller to pay part of them when you write your offer. In a cooling market, more sellers are willing to help with that.

And yes, you still want an emergency fund. Ideally, 3 to 6 months of living expenses. That is a big ask for a lot of people, but you do want some money set aside because homeownership comes with surprises.

To estimate affordability, use the 28% rule. No more than 28% of your gross monthly income should go toward housing.

Example:

- $120,000 annual household income

- $10,000 gross monthly income

- 28% of that = $2,800

That means your monthly payment for principal, interest, taxes, and insurance, often called PITI, should stay around or below $2,800.

Hire The Right Realtor For Moving To Omaha

If you are moving to Omaha, do not wait until after you fall in love with a house to find an agent. Get the right Realtor lined up first.

Ask friends, family, or coworkers for referrals. Interview at least three local agents. What you want is:

- Local experience and expertise

- Someone you trust

- A personality fit

- A full time professional

This is not the time to hire your part time relative who does real estate on the side.

Vet agents online too. Look at Zillow reviews. Google their name. Read what people are saying.

Here are a few smart questions to ask:

- How long have you been working as a real estate agent?

- Are you full time or part time?

- Are you familiar with the areas I am interested in?

- What is your commission or compensation policy?

- What happens if I am not satisfied with your services?

One major change to know about. As of August 17, 2024, before an agent can show you a home, you are required to sign a buyer broker agreement.

Read that agreement carefully before signing anything. Pay attention to:

- How long the contract lasts

- How the agent gets paid

- Your obligations

- The agent's duties

The length of the contract is negotiable.

Compensation is negotiable too. There is no such thing as a standard commission.

And be careful with online leads. If you click around on Zillow and call the name attached to a listing, you may end up routed to a newer team member rather than the experienced agent whose ad you saw. Nothing wrong with new agents, but you should know who you are actually hiring before you sign anything.

Get Preapproved The Right Way

The next step is getting preapproved with a reputable local lender. Not all lenders are created equal, and if you are moving to Omaha, a lender who understands the local market can make the process smoother.

Lenders are mainly looking at three things:

- Credit

- Assets

- Income

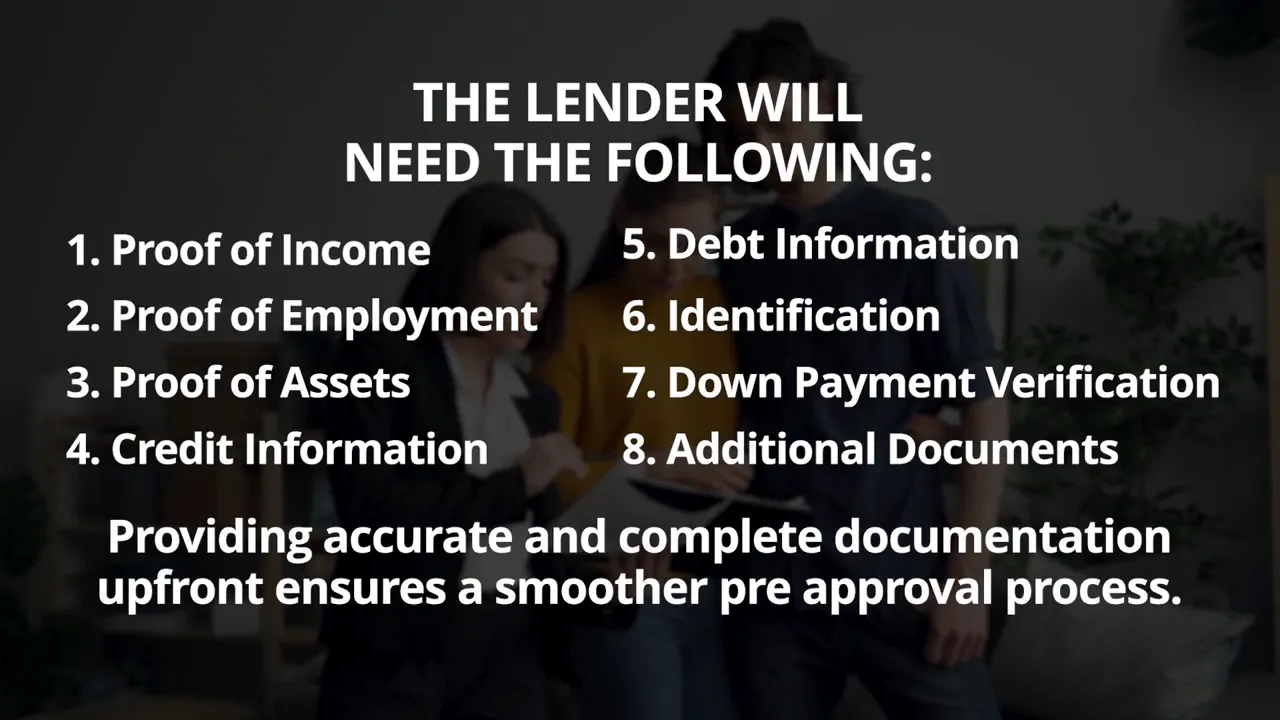

Be ready to provide:

- Recent pay stubs

- W2s from the last two years

- Tax returns

- Employment verification

- Bank statements

- Investment account statements

- Permission to pull your credit

- Debt information

- Government issued photo ID

- Proof of funds for your down payment

- Any extra documents tied to divorce, bankruptcy, child support, or rental income if applicable

If you shop several lenders within a 30 day window, the credit pulls generally count as one inquiry for scoring purposes, so do not be afraid to compare options.

Depending on your situation, you may qualify for:

- FHA for lower credit scores or smaller down payments

- VA for eligible veterans, often with no down payment and no mortgage insurance

- USDA for qualified rural areas, often with no down payment

- Conventional for stronger credit and more flexibility

Here is the caution a lot of buyers miss. Just because a lender approves you for a certain amount does not mean you should spend that amount.

Your principal and interest may stay fixed on a 30 year fixed loan, but your taxes and insurance can still increase over time. That monthly payment is not as frozen as many people think. Leave room in the budget.

House Hunting Strategy For Moving To Omaha

House hunting gets emotional fast, especially if you are moving to Omaha and trying to learn neighborhoods at the same time. The key is to stay grounded.

Start with a list of must haves versus wants. The perfect home does not exist.

A good rule of thumb is to grade each home on a scale of 1 to 10. The perfect 10 is probably out of your budget. What you are really looking for is an 8 out of 10.

That means:

- 80% of your needs are met

- 10% can be changed

- 10% you can live with

See homes in person. Good homes move quickly, so when a strong property hits the market, you want to move.

Also, look past cosmetics. Paint colors, decorating, and staging are temporary. What you are really buying first is location.

Think about resale while you buy. Maybe you are personally okay with a house on a busy street. Fine. But when you go to sell, that busy street may cost you.

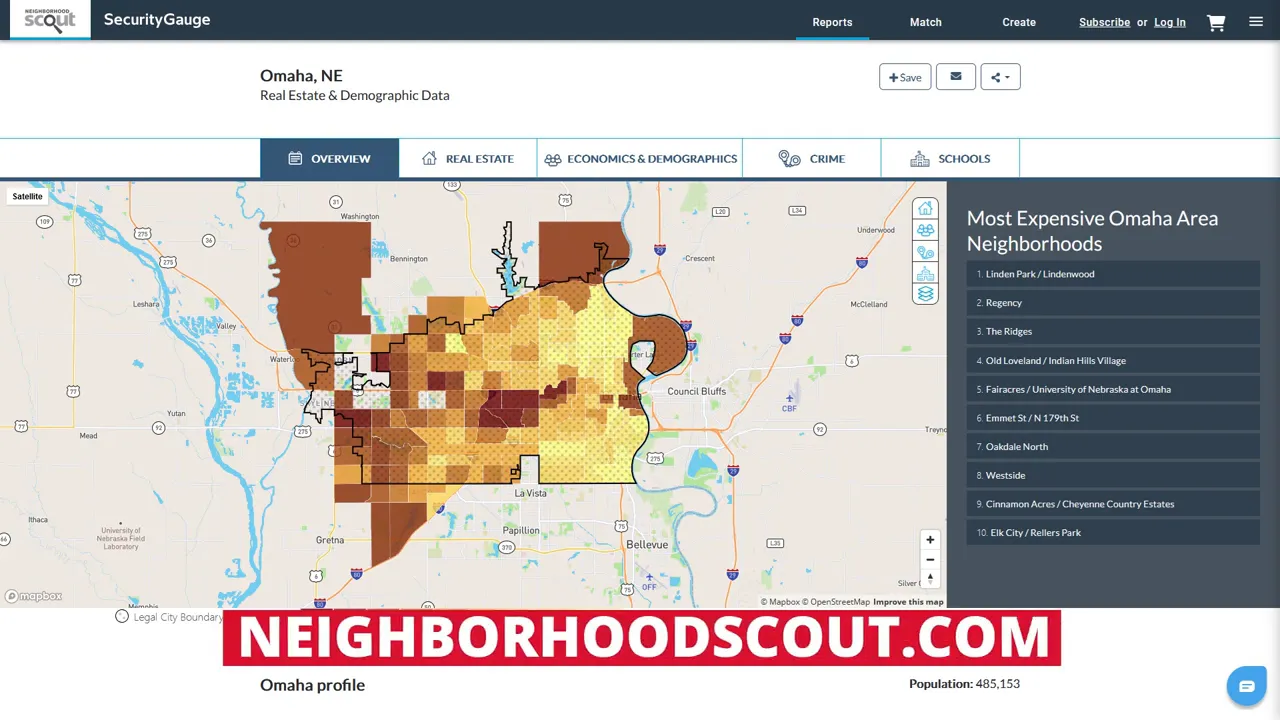

In Omaha, school districts matter. Even if you do not have kids, they can affect future value and buyer demand.

You should also research crime patterns and surrounding area data.

And yes, check the state sex offender registry by location as part of your due diligence on the neighborhood.

Make A Smart Offer Without Overcomplicating It

Once you find the right home, do not drag your feet. There is an old saying in real estate that fits pretty well here: if you sleep on it, you might not sleep in it.

Now, what should you offer? That part is up to you. Your agent can provide market data and comparable sales, but they cannot decide the number for you.

Before you sign any offer, read the contract.

You will also usually submit an earnest deposit. This is money that shows the seller you are serious about buying. The amount is negotiable, but on a $300,000 home, 1% is common. That would be $3,000.

The earnest money is held in escrow by the title company and credited back to you at closing.

After you submit an offer, the seller has three choices:

- Accept it

- Reject it

- Counter it

If they reject it, you can write another offer or move on.

If they counter, you can accept, counter back, or walk away.

Another point people ask about all the time is how the buyer's agent gets paid. The buyer's agent can ask the seller to pay that compensation as part of the contract, and again, compensation is negotiable.

Protect Yourself During Due Diligence

This is where you make sure you are not buying a money pit with a nice kitchen.

In the purchase agreement discussed here, the buyer has 14 calendar days to conduct inspections if they choose to do them. This is the due diligence window.

Possible inspections include:

- Whole house inspection

- Sewer scope

- Radon test

- Mold test

- Structural engineer inspection

- Any other inspection you believe is necessary

The buyer pays for inspections at the time they are performed, so order them quickly after the contract is accepted.

For older homes with mature trees, a sewer scope can be a very smart first move.

If that checks out, then move into the full home inspection.

In Omaha and eastern Nebraska, radon is a big deal. This area is known for some of the highest radon levels in the country. Radon is a colorless, odorless radioactive gas that comes from the breakdown of uranium in soil, and it can accumulate inside homes.

It is also the second leading cause of lung cancer behind smoking. So yes, a radon test matters.

If radon is found, the buyer can ask the seller to install a radon mitigation system.

Once inspections are complete, you have three options:

- Accept the home as is

- Ask the seller to make repairs

- Bail during the inspection window

That is why this step matters so much. If you are going to walk, this is usually the window to do it.

During escrow, which is often around 30 days, the title company handles the title search and the lender works toward final loan approval. You will also need homeowner's insurance, and in Nebraska you need to pay attention because rates are often higher than average.

One major insurance issue to watch is the age of the roof. An older roof may be harder to insure or may not qualify for full replacement coverage.

You will also need to set up utility transfers before closing.

Understand The Appraisal Process

An appraisal is simply an opinion of value. The lender may require one depending on your financing and down payment.

The lender has you pay for the appraisal upfront because they are protecting their investment. They do not want to loan $300,000 on a house that is not worth $300,000.

If you are using government backed financing like FHA or VA, the property generally needs to appraise at or above the purchase price and meet certain condition standards. Safe, secure, and sound is the idea.

That means the lender may require repairs before closing. A classic example is a missing handrail on a stairwell.

Do A Thorough Final Walkthrough

The final walkthrough usually happens 24 to 48 hours before closing. This is not just a formality. It is your last chance to verify the property is in the condition you agreed to buy.

Your goals during the final walkthrough are to:

- Confirm the overall condition

- Check that agreed repairs were completed

- Verify fixtures and appliances included in the sale are still there and functioning

- Make sure there is no new damage

- Confirm the property has been vacated and left broom clean unless otherwise agreed

Notice the wording there. Broom clean. Not perfect. Not deep detailed spotless. Just reasonably clean and emptied out as agreed.

Bring these items with you:

- Contract

- Inspection report

- Checklist

- Phone or camera for notes and photos

Close The Right Way And Avoid Fraud

Closing day is when ownership officially transfers from the seller to the buyer. This is the finish line.

Before closing, review the closing disclosure carefully. It outlines the costs and payments connected to the purchase.

Bring a current government issued photo ID.

Bring the required funds in the correct form, usually a certified check or wire transfer. Personal checks are typically not accepted.

And here is a huge one. Never trust wire instructions sent only by email. Wire fraud is real. Always verify wiring instructions directly with the title company or the appropriate party through a trusted method before sending any money.

Closing usually takes about an hour and often happens at the title company.

Typical closing day activities include:

- Signing final documents

- Paying remaining closing costs and down payment funds

- Title transfer

- Funds distribution

- Key exchange

After closing, keep your documents for tax purposes and future reference. Verify the deed gets recorded. And once the keys are in your hand, change the locks.

If you are moving to Omaha, buying a home here can absolutely be done with confidence. The biggest difference between a smooth transaction and a stressful one usually comes down to preparation. Know your numbers, hire the right people, read what you sign, inspect thoroughly, and stay alert all the way through closing.

That is how you turn homeownership from overwhelming into manageable.

If you want help mapping out your numbers, finding the right neighborhoods, and avoiding common first-time buyer mistakes, reach out today. Call or text me at 402-490-6771 to start planning your Omaha home purchase.

FAQ

How much money do I need when moving to Omaha to buy a home?

You should plan for three buckets of money: down payment, closing costs, and an emergency fund. A common example on a $300,000 home is $10,500 down with FHA financing plus about $9,000 in closing costs if you estimate 3%.

Is moving to Omaha a good time to ask a seller to pay closing costs?

It can be. In a cooler market, more sellers may be open to helping with buyer closing costs. That request can be written into the offer.

What is the 28 percent rule in an Omaha homebuying guide?

It is a budgeting rule that says no more than 28% of your gross monthly income should go toward housing costs, including principal, interest, taxes, and insurance.

Do I need a buyer broker agreement before seeing homes?

Yes. As described here, before an agent can show a home, a buyer broker agreement is required. Read it carefully and pay attention to contract length, duties, and compensation.

Why is radon such a big deal when moving to Omaha?

Eastern Nebraska is known for high radon levels. Since radon is a colorless, odorless radioactive gas and a major health risk, a radon test is an important part of due diligence.

What should I bring to the final walkthrough?

Bring the contract, inspection report, a checklist, and your phone or camera so you can verify condition, repairs, fixtures, and any new damage before closing.