Home buying questions are everywhere. If you are pregnant with doubts, unsure when to pull the trigger, or simply want to make smarter choices, this guide walks through the ten most searched home buying questions and gives straightforward answers you can use today.

Every section below answers a key home buying question, explains the reality behind common advice, and offers practical next steps. Expect clear definitions, example calculations, and checklists you can act on. The goal is to turn confusing online noise into a plan you can follow.

Table of Contents

- 1. Is it better to buy or rent?

- 2. What are the steps in buying a home?

- 3. How do interest rates affect buying a home?

- 4. How much should I save for a down payment?

- 5. When is the best time to buy a home?

- 6. How can I improve my credit score to buy a home?

- 7. What are the hidden costs for buying a home?

- 8. How do I select the right real estate agent?

- 9. What should I look for during a home inspection?

- 10. What are the tax benefits of owning a home?

- Practical checklist: Before you make an offer

- Common mistakes people make when answering these home buying questions

- Quick resources

- FAQ

1. Is it better to buy or rent?

This is the #1 home buying question for a reason: the right answer depends on your finances, timeline, and personal situation. There is no universal truth that buying is always better than renting. What matters is whether buying fits your current financial position and future plans.

Key financial items to check

- Down payment savings — Do you have money for a realistic down payment for your market?

- Closing costs and reserves — Beyond the down payment, can you cover closing costs and have an emergency reserve for repairs?

- Debt and income stability — How much consumer debt do you have? How steady is your income or job history?

- Time horizon — Can you reasonably plan to stay in the home at least five years?

If you do not have emergency savings or you expect to move within a few years, renting can be the smarter move. If you have stable income, a reasonable down payment, and plan to stay put, buying is often a better long term financial decision.

Seller credits and creative structuring

If down payment or closing costs are a concern, certain offer structures can help. For example, on a $300,000 purchase you could offer a higher purchase price and request the seller pay some or all of the closing costs. That shifts cash at closing but increases your loan or purchase price, so make sure the numbers still make sense long term.

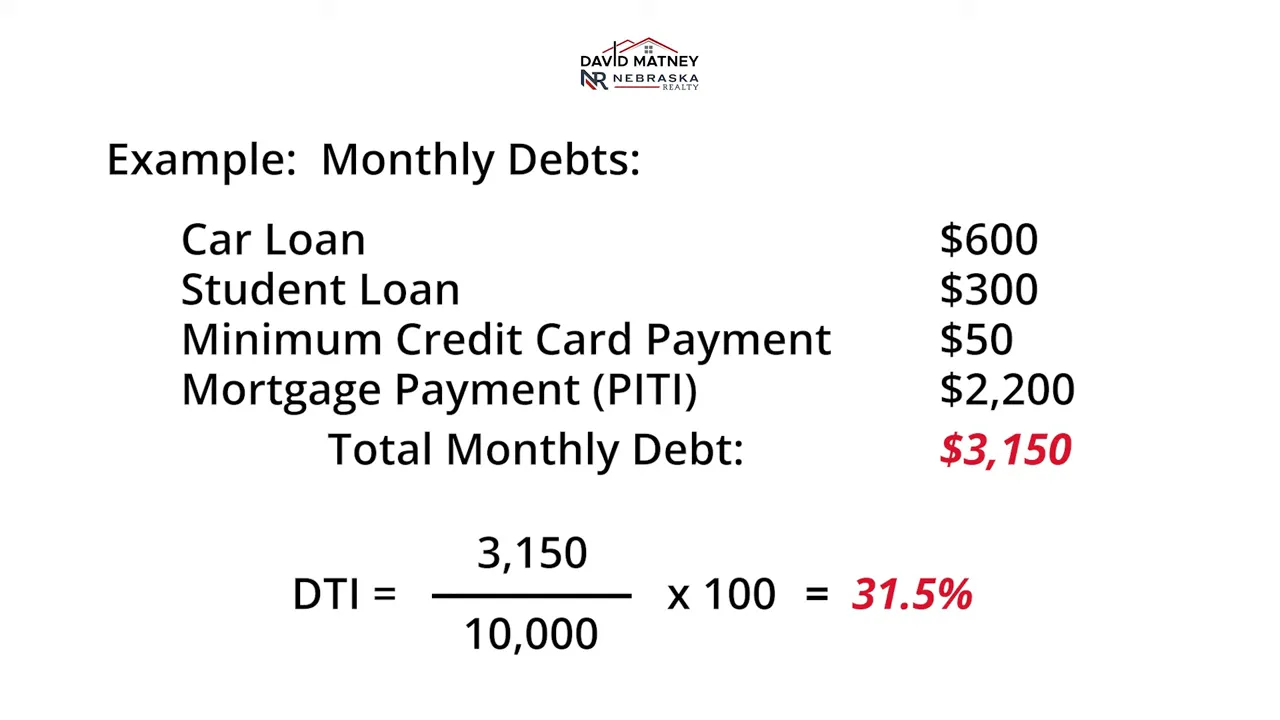

Debt-to-income (DTI) matters

Lenders use debt-to-income to assess affordability. The formula is:

DTI = (total monthly debt payments / gross monthly income) × 100

Example: monthly debts of $600 (car) + $300 (student loan) + $50 (credit card minimum) + $2,200 (mortgage PITI) = $3,150 in monthly debt. If your gross annual income is $110,000, your gross monthly income is about $9,166. The DTI would be roughly 34.4%. Most lenders prefer DTI below 43%, with lower being better.

2. What are the steps in buying a home?

That is one of the central home buying questions because having a roadmap calms anxiety and prevents costly mistakes. In short, the major steps are:

- Get preapproved by a lender so you know your budget and loan options.

- Work with an agent to identify neighborhoods and homes that meet your needs.

- Make an offer and negotiate terms, contingencies, and the closing date.

- Complete inspections and negotiate repairs or credits if problems appear.

- Finalize mortgage underwriting, clear conditions, and close the transaction.

Each step has sub-steps (earnest money, appraisal, title work) but knowing this flow helps you track progress and deadlines.

3. How do interest rates affect buying a home?

One of the most frequent home buying questions is how much rates matter. Short answer: a lot. Mortgage interest rates dramatically change your monthly payment and your buying power.

Illustration: on a $300,000 loan

- At 7% interest, a 30-year fixed principal and interest payment is about $1,997 per month.

- At 4% interest, the same loan’s principal and interest payment is about $1,432 per month.

When rates rise, monthly payment and total borrowing cost increase, reducing how much home you can afford. Rates are set by market forces, especially the bond market, and nobody can predict them with certainty. The best rule: focus on what you can afford at today's rates and make a plan rather than trying to time the market.

4. How much should I save for a down payment?

This is a core home buying question with multiple valid answers depending on loan type and goals.

20% down avoids private mortgage insurance and gives you the most favorable financing, but it is out of reach for many buyers.

Alternative programs:

- FHA loans — Require 3.5% down and are more forgiving on credit. Example: on a $300,000 purchase, 3.5% down equals $10,500.

- VA loans — For eligible veterans and some military spouses, VA offers 0% down and no mortgage insurance. Extremely powerful when you qualify.

- USDA loans — Designed for eligible rural and suburban areas, USDA can offer zero down for qualified buyers with income limits.

Which route to take depends on your situation: if you have resources to put 20% down and want lower monthly payments and no PMI, that’s ideal. If not, government-backed or other low-down options can get you into a home sooner while you build equity and savings.

5. When is the best time to buy a home?

This is one of the most searched home buying questions because timing feels risky. The best time to buy a home is when you are financially ready and your lifestyle fits homeownership. There is no perfect month or market cycle that fits everyone.

Real advice: stop trying to time the market and focus on readiness. If you want long-term stability and will be in the home for several years, buying now may be better than waiting indefinitely for an "ideal" moment.

6. How can I improve my credit score to buy a home?

Credit score matters for interest rates and loan access, so this home buying question is important. Here’s a practical plan:

- Get your free credit reports from annualcreditreport.com and dispute errors.

- Keep balances low — aim below 30% of each card’s limit.

- Pay on time — payment history has the largest impact on score.

- Don’t open new accounts just before applying for a mortgage.

- Keep older accounts open to help average account age.

- Reduce outstanding debt when possible — pay down personal loans, auto loans, and high-rate accounts.

- Talk with a lender early — they can build a plan tailored to your credit and goals.

7. What are the hidden costs for buying a home?

Along with the down payment, ask about closing costs, but don’t stop there. Hidden costs commonly surprise buyers who only budget for the mortgage and down payment.

Common items to plan for:

- Closing costs — usually 2% to 5% of purchase price (earnest deposit, origination fees, appraisal, title insurance, escrow fees, prepaid taxes and insurance, inspections).

- Moving costs — movers, truck rental, packing, time off work.

- Appliances and window coverings — builders may not include them; replacing can cost thousands.

- Landscaping — new lawns, patios, fences often are buyer expenses on new construction.

- Furniture and setup — relocating buyers often spend several thousand furnishing a new place.

- Immediate repairs or upgrades — painting, cleaning carpets, fixing older systems.

- Future replacements — HVAC, roof, windows are large line items buyers should budget for if they are aged.

Bottom line: build a realistic budget that includes closing costs plus a reserve for the first 6 to 12 months of ownership. That answers a frequent home buying question about "how much cash do I need" more accurately than a single number.

8. How do I select the right real estate agent?

Picking an agent answers more than one home buying question at once: it affects your search, offer strength, and closing experience. Here is a practical approach.

Understand roles

- Buyer agent finds homes, negotiates your offer, and guides inspections and paperwork.

- Listing agent represents sellers and markets homes for sale.

Where to find agents

- Ask friends and family for referrals.

- Check online reviews and listings on Zillow, Realtor.com, and Google.

- Look at an agent’s social media or YouTube channel — it reveals knowledge and personality.

Interview multiple agents

- Ask experience, recent sales, and whether they work full-time or part-time.

- Check the multiple listing service for their track record and current listings.

- Request references from past clients and contact them.

- If you don’t have an agent yet, book a call with me and let’s strategize: Schedule a free consultation.

Commission and important changes

Agent compensation is negotiable. Recent legal settlements changed how commissions are shown in MLS and introduced buyer broker agreements. Before touring homes, you may be asked to sign a buyer broker agreement outlining fees, term, and duties. You can still ask the seller for a credit to cover buyer agent costs, depending on market conditions.

Red flags include poor communication, pushy sales tactics, lack of local market knowledge, and no recent transactions.

9. What should I look for during a home inspection?

A home inspection is not a pass/fail test; it is an information gathering exercise. The inspection highlights safety issues and major material defects you should know about before closing.

Priority systems to review:

- Roof condition and expected remaining life

- Foundation issues and signs of movement

- Electrical wiring and panel condition

- Plumbing condition and sewer line concerns

- HVAC system age and service history

Depending on the property and area, add specialty inspections: sewer scope, radon test, foundation engineer review, mold, or septic inspections. In some local contracts, buyers have a set number of days for inspections — for example, a 14-day inspection period is common in certain markets — so plan accordingly.

10. What are the tax benefits of owning a home?

Owning a home can offer meaningful tax benefits that often show up as lower reported taxable income or exclusion of gains when selling.

- Mortgage interest deduction — interest on mortgage debt can be deductible subject to current tax rules and loan limits.

- Property tax deduction — property taxes may be deductible within limits and subject to local law changes.

- Capital gains exclusion — when you sell a primary residence, you may exclude a portion of the gain (subject to rules and time ownership/residence requirements).

Always consult a qualified tax advisor to understand how these home buying questions apply to your particular tax situation.

Practical checklist: Before you make an offer

- Get preapproval from a reputable lender and know your interest rate options.

- Confirm how much you can afford including taxes, insurance, HOA, and maintenance.

- Save for closing costs, moving, and an initial emergency reserve.

- Interview and sign with a buyer agent so you have representation.

- Plan inspections and budget for potential repairs or replacements.

- Ask the seller for credits if you need help with closing costs, but run the numbers first.

Common mistakes people make when answering these home buying questions

- Underestimating maintenance and replacement costs for systems like HVAC and roof.

- Using annual income instead of monthly income when calculating DTI.

- Skipping a full inspection to "save money" — that almost always backfires.

- Assuming the seller will always pay closing costs — sometimes they can, sometimes not.

- Over-extending on the mortgage because of low rates without budget for taxes and insurance increases.

If you'd like personalized help—reviewing your budget, getting preapproved, or finding the right home—I can help. Book a free consultation: Schedule a call.

FAQ

How many of these home buying questions should I answer before I start touring houses?

You should have at least a preapproval, a clear budget, and an agent lined up before touring. That will save time and prevent falling in love with homes you cannot afford.

Can I buy with less than 20% down without getting a bad mortgage?

Yes. Programs like FHA, VA, and USDA allow lower or no down payment. Keep in mind lower down payment often means mortgage insurance or other costs. Run the numbers to compare monthly costs and long-term benefits.

Is it better to pay points to lower my interest rate?

Paying points makes sense if you plan to keep the loan long enough to recoup the upfront cost through lower monthly payments. Ask your lender for a break-even analysis to decide.

What should my emergency reserve be after buying?

A common recommendation is 3 to 6 months of living expenses, but at minimum have a few thousand dollars earmarked for urgent home repairs. Larger, older houses may need a bigger reserve.

How long does the mortgage approval process typically take?

From preapproval to closing, typical timelines vary by lender and market. After you have an accepted offer, underwriting and closing usually take 30 to 45 days, assuming no surprises.

Will a seller pay for my buyer agent?

Traditionally sellers offered commission splits, but market and legal changes mean compensation is negotiable. You can request a seller credit to cover buyer agent costs, but it depends on negotiations and market conditions.

How do interest rates and home prices interact?

Higher interest rates reduce buyers' monthly affordability, which can put downward pressure on prices in some markets. Conversely, lower rates increase buying power and can push prices up. Focus on affordability for your budget rather than predicting precise market moves.

For anyone wrestling with these home buying questions, the best strategy is pragmatic preparation: get your finances in order, educate yourself about loan programs that fit your profile, interview agents, and build a reserve for the unexpected. That approach answers the most important home buying questions with clarity you can act on.