The 2026 housing market is shaping up to be a year of normalization rather than drama. After an intense 2025 where sales, prices, and inventory all rose while interest rates edged down, the question many people keep asking is the same: what does the 2026 housing market mean for buyers, sellers, and anyone thinking about moving to Omaha? This piece breaks down the forces that matter, realistic forecasts for inventory, prices, and rates, and practical steps you can take whether you plan to buy or sell in the next 12 months.

Table of Contents

- 2025 Omaha Real Estate Market Recap

- Why Affordability Is Shaping Omaha’s 2026 Housing Market

- Politics, Policy & What They Mean for Omaha’s 2026 Housing Market

- Inventory, Prices & Rates: What to Expect in Omaha’s 2026 Market

- Jobs, Inflation & How Omaha’s Economy Impacts the 2026 Market

- Practical Advice for Omaha Homebuyers in 2026

- Practical Advice for Omaha Home Sellers in 2026

- Omaha Housing Market Numbers & Forecasts for 2026

- Common Mistakes to Avoid in Omaha’s 2026 Housing Market

- Final Thoughts: How to Think About Omaha’s 2026 Housing Market

- Frequently asked questions

2025 Omaha Real Estate Market Recap

2025 was an unusual year in many ways. Sales were up, prices were up, inventory increased, and interest rates began trending downward. Those trends moved the local market closer to what industry pros call a normal market. Normal means fewer bidding wars, more inspection contingencies honored, and more time for buyers and sellers to make reasoned decisions. The transition away from the extreme demand seen during the pandemic era is the foundation for how the 2026 housing market will behave.

The runup during the COVID years created a housing imbalance: too much demand, too little supply, and rapid price appreciation. That imbalance contributed to broader inflation. The response came from the monetary side: interest rates rose sharply, killing demand quickly and dropping sales volumes. Importantly, that drop was a sales crash, not a price crash. Prices held, while transaction counts fell. That distinction shapes how the 2026 housing market will evolve: stabilization, not collapse.

Why Affordability Is Shaping Omaha’s 2026 Housing Market

Affordability is the single greatest limiter on who can participate in the 2026 housing market. Higher interest rates and higher prices pushed many potential buyers to the sidelines. Nationwide trends also show the median age of first-time buyers increasing: more buyers are older and better capitalized. In Omaha, the same pressures exist — buyers need more savings and higher incomes to qualify.

Supply and demand still rules: the market needs time to rebalance. Time allows wages to catch up, inventory to replenish, and builders to recalibrate product mix. Builders respond to affordability constraints by changing what they build. Instead of larger, higher-priced homes, builders often pivot to slightly smaller footprints that hit price points buyers can reach. That "shrinkflation" in new construction is already visible and will continue influencing the 2026 housing market.

Politics, Policy & What They Mean for Omaha’s 2026 Housing Market

Public policy and political cycles matter for the 2026 housing market. Election years change priorities and rhetoric, and policy proposals can ripple quickly through mortgage markets. Ideas like portable mortgages, relaxed credit requirements, or extremely long-term loans sound appealing because they promise increased affordability. But these solutions increase demand, and when demand rises faster than supply, affordability worsens again.

Tariffs and building costs: policy choices at the national level can also affect construction prices. Tariffs on essential inputs such as lumber increase builders’ costs, which are passed to buyers. In Omaha, builders reacted in 2025 to tariff announcements by raising prices. Expect similar sensitivity in 2026 if tariffs or supply constraints return to the conversation.

Inventory, Prices & Rates: What to Expect in Omaha’s 2026 Market

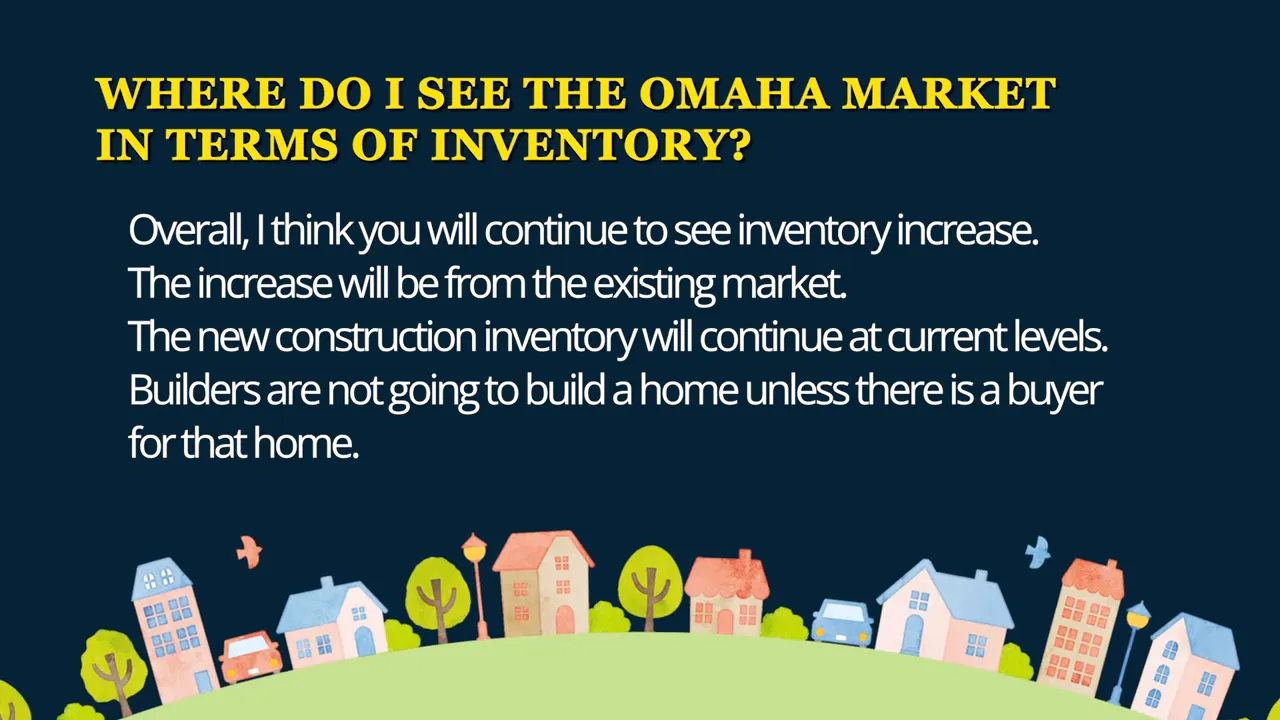

Inventory will be a defining variable in the 2026 housing market. Here is how those three pieces are likely to interact:

- Inventory: Expect inventory to continue increasing, primarily from the existing home side. As interest rates trend lower, more sellers who have been waiting will list their homes. I estimate about a 15 percent increase in existing inventory across the Omaha region. New construction inventory will remain disciplined; most builders do not want empty spec homes, so new build inventory might tick up only 2 to 3 percent.

- Prices: New construction prices are likely to remain flat to slightly up, perhaps 0 to 1 percent, as builders adjust home sizes. Existing home prices may rise moderately, roughly 3 to 3.5 percent. A price crash is unlikely in Omaha — instead expect gentle appreciation as inventory growth meets steady buyer demand.

- Interest rates: Rates are the wildcard. If inflation cools and growth slows, rates should ease. I expect mortgage rates to average in the mid to high 5s early in the year and drift toward the high 5s or low 6s as inflation stabilizes. That change will be slow and subject to national monetary policy decisions.

These interactions mean the 2026 housing market in Omaha will be more buyer-friendly than the frenzy years, but still not a bargain basement environment. Buyers will have more choices but still need to budget carefully. Sellers will need to be realistic about pricing and condition to hit the market successfully.

Jobs, Inflation & How Omaha’s Economy Impacts the 2026 Market

Employment, inflation, and the Fed’s response have a direct impact on mortgage rates and buyer confidence. If unemployment ticks up and growth softens, the Fed may lower the federal funds rate, which tends to push mortgage rates down. I expect inflation to run slightly above the 2 percent target in early 2026, perhaps in a 2.8 to 3.4 percent range. That is not disastrous, but it may keep rates higher than the optimistic 4 percent scenarios some hope for.

What this means for the 2026 housing market is simple: slight cooling of inflation plus softer employment gives the Fed room to ease. Easing encourages sellers to list and buyers to act. But the timing is uncertain, so plans should include flexibility.

Practical Advice for Omaha Homebuyers in 2026

If you plan to buy in the 2026 housing market, preparation and realism will be your greatest advantages.

- Get your finances in order: save for a down payment, understand your debt-to-income ratio, and improve your credit profile. Lenders remain careful, and qualifying standards will matter.

- Have a plan, not a panic: waiting for a dramatic crash is a risky strategy. Instead, decide what compromises you can accept: location tradeoffs, smaller square footage, or a fixer-upper you can improve over time.

- Use the increased inventory to your benefit: with more options, you can afford to be selective about inspection contingencies and negotiate reasonable contingencies that protect you.

- Think long term: housing is a long-duration investment. If you plan to be in a home for several years, small price fluctuations matter less than your monthly carrying costs and quality of life.

Practical Advice for Omaha Home Sellers in 2026

Sellers face a market where buyers have more leverage than in the frenzy years. Winning strategies will return to basics:

- Price it right: homes priced competitively in the current market will get more attention and sell faster. Expect sale prices close to list, typically in the 98 to 99 percent range.

- Stage and prepare: declutter, deep clean, service HVAC systems, and make necessary repairs before listing. Buyers will negotiate on issues they find; pre-empt those negotiations by fixing them in advance.

- Be proactive: understand local comparables and market conditions. If multiple offers are unlikely, focus on getting the highest qualified offer by presenting your home as move-in ready.

Omaha Housing Market Numbers & Forecasts for 2026

Predictions are always guesses, but making informed assumptions helps planning. Here are practical projections for Omaha based on current trends and reasonable macro scenarios:

- Sales volume: expect sales to rise about 7 percent year over year, putting total transactions near 13,200 for the metro area.

- Inventory: existing inventory up roughly 15 percent; new construction inventory up 2 to 3 percent.

- Prices: existing home prices up around 3 to 3.5 percent; new construction flat to +1 percent.

- Mortgage rates: average mortgage rates in a range near 5.75 to 6.5 percent, trending slightly lower as the year progresses if inflation cools.

- Inflation: in the 2.8 to 3.4 percent range — not ideal, but manageable.

These numbers describe a steady, normalizing 2026 housing market rather than a volatile one. Markets will vary locally; some neighborhoods and price tiers will behave differently. The national picture may show weak price growth overall, perhaps around 2 percent, while local markets like Omaha outperform modestly.

Common Mistakes to Avoid in Omaha’s 2026 Housing Market

As the 2026 housing market settles, avoid quick fixes that look attractive but add risk:

- Do not rely on creative financing that stretches affordability without addressing income and savings needs.

- Avoid assuming a policy change will instantly solve affordability — measures that increase demand without adding supply make long-term affordability worse.

- Do not ignore the fundamentals: creditworthiness, realistic budgets, and home condition matter more than flashy headlines.

Final thoughts

The 2026 housing market will be a return to a healthier pattern: more inventory, steady sales, moderate price growth, and rates that slowly become more favorable as economic signals justify easing. Omaha’s stable economy, quality of life, and cost advantages position the local market to perform well compared with many coastal metros.

Whether you are buying or selling, prioritize planning over panic. Homes are long-term decisions. Play the long game and align your timing with personal readiness and finances rather than headlines. Real estate is local, and in a steady market like Omaha the right preparation often produces winning outcomes.

If you need help navigating the 2026 Omaha housing market or have questions about your specific situation, please reach out — I’m happy to help. Call or text me at (402) 490-6771 to discuss strategy, timing, or to get a personalized market review. I’ll help you make a clear plan whether you’re buying, selling, or just weighing your options.

Frequently Asked Questions About Omaha Real Estate Market

How will interest rates affect the 2026 housing market in Omaha?

Mortgage rates are the primary demand lever for the 2026 housing market. If inflation cools and employment softens, the Fed may ease policy, putting downward pressure on mortgage rates. Expect rates to average in the high 5s to low 6s with a gradual downward bias if macro conditions permit.

Will home prices crash in 2026?

A crash in Omaha is unlikely. The 2026 housing market is expected to show modest price gains: roughly 3 to 3.5 percent for existing homes and flat to minimal increases for new construction. Local variations can occur, but widespread price declines are not the base case for Omaha.

Is now a good time to buy in the 2026 housing market?

Buying should be based on personal readiness and financial stability rather than timing the market. The 2026 housing market will offer more inventory and negotiation room than the frenzy years, so buyers who are prepared financially and willing to compromise on features or location can find good opportunities.

What should sellers do to succeed in the 2026 housing market?

Sellers should focus on correct pricing, staging, and pre-listing repairs. With a more balanced market, homes that are clean, well-maintained, and priced appropriately will attract qualified buyers and close near list price.

How will new construction impact the 2026 housing market?

Builders will continue to be cautious. New construction inventory will likely remain controlled, and builders will adjust product sizes to hit affordability targets. Expect new home prices to be flat to slightly higher while builders shrink average square footage to meet buyer needs.